Data calls and stat reporting continue to remain a slow, tedious, and error-prone overhead to most carriers. Recent advances in technology have demonstrated that streamlining and automating this can provide benefits beyond meeting regulatory requirements. Join us in building a community that puts data to work beyond staying in compliance.

Insurance is a data-driven industry. Well before this became a technology-driven buzzword, insurance carriers and regulators have been building on the work of James Dodson since 1762. History aside, state laws in the U.S. today give insurance regulators the responsibility to oversee the operation of insurers. They are tasked with the responsibilities to:

• Ensure rates meet statutory standards, i.e., rates are not inadequate, excessive, or unfairly discriminatory.

• Monitor the market structure and performance. They are required to act if necessary to restore competition or remedy problems caused by market failure.

In the property and casualty insurance market, there needs to be a constant flow of information from the carriers in the form of stat reporting and data calls. This information becomes the basis for regulators' evaluation of solvency, market trends, and relationships between rates and coverages. Thus, carriers are required by law to prepare and submit extensive statistical and financial reports to the state insurance department.

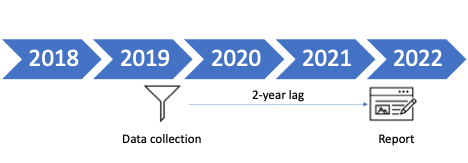

Keeping the focus on Auto Insurance, though this could be extended to other lines, the information collected by regulators is published in the annual Auto Insurance Database report. This report, which was published in January 2022, covers experience up to December 2019. Whereas the publication from the National Association of Insurance Commissioners (NAIC) lags the experience by three years.

Long Lags in Market Publication

While statistical agents can produce reports using an annual, quarterly, or accelerated reporting basis, most carriers prefer the annual basis due to the overhead associated with collecting, cleaning, aggregating, and processing data. This has led to resistance from the industry in shortening the recommended report date. In the larger scheme of things, this data is insufficient to help inform policy decisions leading to data calls that add overhead to an already strained system performing similar tasks on more focused, time-bound segments of data.

Both the industry and regulators would like to see more timely, accurate, and higher granularity data with reduced overhead in managing the process.

Benefits of Timely and Frequent Market Reports

The Auto Insurance Database report contains detailed premium, loss, operations, and market condition information by state. By leveraging the trends and performance by coverage areas, carriers can benchmark their own performance compared to the market as a whole and make critical decisions. From pricing and operational overhead to market entry or exit, leaders can leverage timely data from a trustworthy source to have a sound foundation for decision-making.

While compliance is a necessary overhead, automating the process can only help carriers increase profitability, especially in an environment where prices are regulated and costs soar. With the advent of newer technology, more uses for the data can open up more opportunities and hence improve the top line.

openIDL

The open insurance data link (openIDL) blockchain network is an open-source private permissioned blockchain network that streamlines regulatory reporting and provides new insights for insurers while enhancing timeliness, accuracy, and value for regulators. By participating in the network, carriers create a private vault of policy and claims data that can be used to fulfill stat-reporting requirements. The same data can be used to fulfill data calls and policy validity verification.

The benefits of using blockchain technology are endless. From mileage verification to developing a truly digital policy card, this technology contains the potential to transform insurance while reducing operational costs.