Premium leakage is a critical issue for carriers writing personal auto insurance, particularly with the rising severity of claims. However, by utilizing data and building partnerships with auto manufacturers, data providers, and new insurtech vendors, carriers can take steps to limit exposures due to incorrect mileage and garaged locations. Join us in building a community to solve this problem.

One major contributor to premium leakage is "soft fraud," where drivers under-report miles driven or misrepresent their garaged location. Drivers do not consider “unintentionally” under-reporting miles driven or misrepresenting garaged location to be a serious issue. Both these factors can have severe consequences for both drivers and carriers.

Mileage Impact

In Illinois, for example, this can result in a reduction of premium between 16% to 24% for a 5,000-mile-a-year difference in the 7,000 to 12,000 range. With the average driver driving just over 11,000 miles a year, this issue is widespread and must be addressed by carriers. As you can see, the impact of incorrect mileage for basic coverage is non-trivial in the highly competitive auto insurance market.

In Illinois, for example, this can result in a reduction of premium between 16% to 24% for a 5,000-mile-a-year difference in the 7,000 to 12,000 range. With the average driver driving just over 11,000 miles a year, this issue is widespread and must be addressed by carriers. As you can see, the impact of incorrect mileage for basic coverage is non-trivial in the highly competitive auto insurance market.

Location Impact

Similarly, misrepresentation of garaged locations can also have a significant impact on premiums. Using base rating factors for Illinois, the difference in base costs for basic minimum coverage can be as high as 24.4% between adjacent ZIP codes. This is particularly problematic for carriers in areas where they may be taking on higher risks than the premiums reflect.

In an environment where carriers are forced to reduce the number of rating factors, mileage and garaging ZIP codes can lead to significant premium leakage. Limiting this would require carriers to be savvy in the capturing and use of data along with the infrastructure to make decisions.

Data Sources

Carriers can leverage a variety of data sources to verify mileage and garaged locations, including telematics data from modern cars. However, adoption of these technologies remains slow, as drivers often view them as invasive. To address this, carriers can take a permission-based approach, clearly communicating the purpose and use of the data they collect and gaining consent from drivers. Additionally, carriers can work with vendors to verify data, incorporate data collection into mobile apps, or partner with vehicle manufacturers to include regular sharing of information.

Driver Concerns

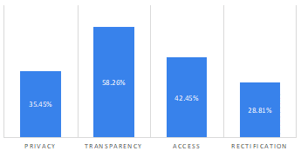

Drivers have several privacy and data usage concerns as described in the Usage Based Insurance report. The number one concern hindering accurate data use in the pricing of insurance policies is transparency. At first glance, drivers conjure up GPS-enabled dongles stuck inside their cars continuously sending information to the cloud. The perceived intrusion seems to be the largest hurdle to overcoming the adoption of technology-driven data collection or verification.

Drivers have several privacy and data usage concerns as described in the Usage Based Insurance report. The number one concern hindering accurate data use in the pricing of insurance policies is transparency. At first glance, drivers conjure up GPS-enabled dongles stuck inside their cars continuously sending information to the cloud. The perceived intrusion seems to be the largest hurdle to overcoming the adoption of technology-driven data collection or verification.

Solution Candidates

Premium leakage is a significant concern for carriers writing personal auto insurance. By utilizing authorized and volunteered data and building partnerships, carriers can address this issue and improve their premium collections by identifying and mitigating the exposures due to mileage and garaged locations.

At our AAIS Pulse: Chicago event in 2022, we realized intrusive, continuous, and real-time monitoring and data collection was far from desirable. Whether you look at it from a consumer lens or a carrier lens, periodic collection of small and relevant exposure data is preferred to vast quantities of granular data. Drivers are more inclined to consent or even voluntarily share data for a well-defined purpose. Depending on the level of sophistication, carriers can choose a path to improve their premium collections based on accurate verified data from a trusted source.

Carriers have options of building features into their own apps, leveraging independent software vendors specializing in customer engagement and data collection, subscribing to data providers, or participating in new and upcoming networks that empower the sharing of information without raw data. While openIDL continues to develop as a single repository for claims and policy data for statistical reporting and data calls, we have the infrastructure for collaboration across networks. openIDL together with MOBI can enable collaboration between auto manufacturers and insurance, solving the mileage and garaged location problems. We can further include leasing and financing organizations to expand the reach of tracking the mileage and ZIP code data on a regular cadence. This could potentially eliminate costs across industries while building an example of a collaborative community helping all participants in the process.