")

As part of the AAIS Webinar Series, AAIS hosted a virtual presentation on June 6, 2023, regarding California’s Mandatory Wildfire Mitigation Credits regulation. AAIS industry leaders, Robin Westcott, Vice President of Government Affairs, Legal & Compliance/General Counsel, Linda Jancik, Product Manager of Personal Lines, Mike Payne, Chief Pricing Actuary, and Matt Hinds-Aldrich, Senior Risk Strategy Lead, presented an overview of how the regulation was addressed across impacted programs from both a product and actuarial perspective. The panel also focused on the consumer notice requirement, highlighting how notice design can help motivate consumer action to complete wildfire mitigations on their properties. Panelists shared a notice template developed in response to this regulation that can easily be used and adapted in response to this regulation.

Overview of the Regulation

In October 2022, the California DOI passed the regulation requiring an insurer to offer specific mitigation factors. Westcott explained that the determination for whether this applied to consumers’ currently filed rate was whether they used the wildfire risk model, or the rating plan segmented a policyholder's rate based upon the policyholder's wildfire risk. “The regulation addresses two types of mandatory mitigation factors as well as the community level and property level mandatory mitigation factors,” Westcott described. “The property level factors cover mitigation measures addressing both the immediate surroundings at the structure, often referred to as ‘defensible space,’ as well as the buildings hardening measures performed on the structure itself.” The regulation further identifies some optional factors relating to wildfire loss that an insurer may incorporate into the rating plans as long as the resulting rate is not excessive, inadequate, or unfairly discriminatory. Westcott shared that throughout the regulation, there are administrative requirements an insurer must follow. “Many of the requirements are around transparency and providing information regarding the mitigation credits to your policyholders,” she said. In addition, each company is still required to make a filing even if your advisory organization has filed with the department.

Wildfire Mitigation in AAIS Manual

Jancik explained that this regulation affected the homeowners by peril (HOBP) and homeowners by composite (HOC) programs at AAIS the most. Filings* were also done for agricultural output, commercial output, and inland marine guide-motor truck cargo. Wildfire risk mitigation credits are available in both California HOBP and HOC programs in the AAIS rule manual as separate rules. “The reason [for this] is that there are different ways of premium determination for these two programs,” Jancik explained. “Because in HOBP, wildfire can be isolated, whereas in HOC, their combined loss costs do not allow it to split up into individual programs.”

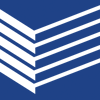

There are three categories of wildfire risk mitigation credits available: community coordination, property hardening, and defensible space. “Whereas the community coordination credit applies to the community you live in, property hardening measures, as well as defensible space measures, can be influenced by the policyholder,” said Jancik. “So, we can't suppress our way out of wildfire.” She believes that communities that are coordinated, collaborative, and consistent in their wildfire mitigation efforts are likely to have lower losses and better outcomes. Property hardening measures relate to all building characteristics that help reduce wildfire risk. The risk of wildfire damage to buildings is also dependent on preventative measures such as ensuring that the area surrounding the building is clear of excessive flammable material and debris.

Rating Impact

For the community coordination credit, AAIS is proposing a 4% wildfire credit for being recognized in a FirewiseUSA site in good standing. “This 4% is larger than most of our other credits,” Payne relayed. “We wanted to recognize that they have a lot of activities going on; they're really committed. So, it was a little bit more robust.” In a California fire risk reduction community, AAIS is proposing a 1% credit. It's a relatively new program, according to Payne, which is why it is different from the FirewiseUSA sites. “But these two pieces are technically mutually exclusive,” he added. “So, you could be in one or both of those types of communities [and] your maximum wildfire credit for community coordination would be 5%.” AAIS is proposing a 1% credit for each of the property hardening credit type activities (Class-A fire-rated roof, enclosed eaves, etc.) “It might seem small, but we really wanted to try and emphasize the fact that when you do more of these, they add up and you'll get more of a benefit,” Payne explained. The same applies for the defensible space credit. “Again, assuming all five activities are met, you would get the 5% compounding impact and you add those together to get a total of 10% for maximum wildfire credit for defensible spaces,” said Payne. “If you add up those three components together, we are proposing a maximum of a 25% credit to the wildfire portion of the loss costs.”

Rethinking Consumer Notices & the AAIS Consumer Notice Tool

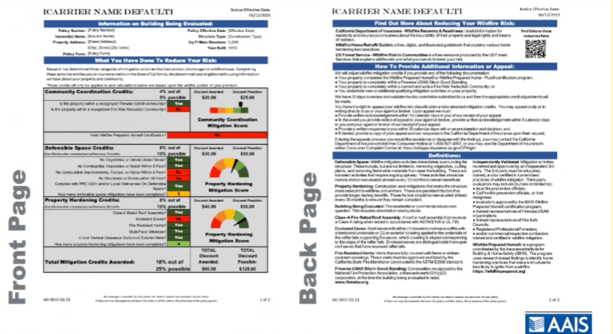

When discussing wildfire mitigation, one of the key factors that comes up is how to incentivize homeowners to take action. “The regulation that's been put forth by CDI goes a long way to start driving change and homeowner behavior,” said Hinds-Aldrich. “But we still need to instill a sense of urgency. [AAIS] discovered the importance of the consumer notice.” Because this regulation puts a lot of focus on actuarial analyses and being compliant with the law, the consumer notice tends to become an afterthought. “[AAIS] started realizing that there's a real missed opportunity here,” Hinds-Aldrich claimed. “So, we spent time developing a consumer notice model.” In doing so, AAIS identified three key issues that needed to be addressed: comprehension, accessibility, and motivation aspects.

When creating the consumer notice sample, AAIS believed that if it was kept short, succinct, and relevant, homeowners would take full advantage of it. Information can either be put in manually through drop-down menus or in an automated fashion at scale. “Whatever the reading is, or variables that are selected, [the form] will automate all of the remaining information,” Hinds-Aldrich explained. The other component worth noting is that this form is entirely customizable by any AAIS member. “Everything can be changed from the colors to the verbiage,” Hinds-Aldrich shared. “[We] recognize that carriers are going to have to make their own choices and may have different variations when they do their own filing.” AAIS has also created a separate version of the consumer notice tool that allows companies that use catastrophic wildfire risk models to disclose the model that was used and how it operates.

If you would like to view the presentation again in its entirety, please click the video above.

Questions? Please don't hesitate to reach out to any of the featured speakers through the contact information below.

Robin Westcott, Esq.

Vice President of Government Affairs, Legal & Compliance / General Counsel

robinw@aaisonline.com

Linda Jancik

Product Manager – Personal Lines

lindaj@aaisonline.com

Mike Payne, FCAS, MAAA

Chief Pricing Actuary

michaelpa@aaisonline.com

Matt Hinds-Aldrich, PhD

Senior Risk Strategy Lead

matth@aaisonline.com

*Note that filings for these programs have not yet been approved.